Most people assume pharmacies make the most money off expensive brand-name drugs. That’s not true. In fact, the opposite is happening: generic drugs are the real profit engine for pharmacies - even though they cost a fraction of brand-name drugs. This paradox lies at the heart of pharmacy economics today, and it’s reshaping who survives in the industry.

Why Generics Are the Hidden Profit Engine

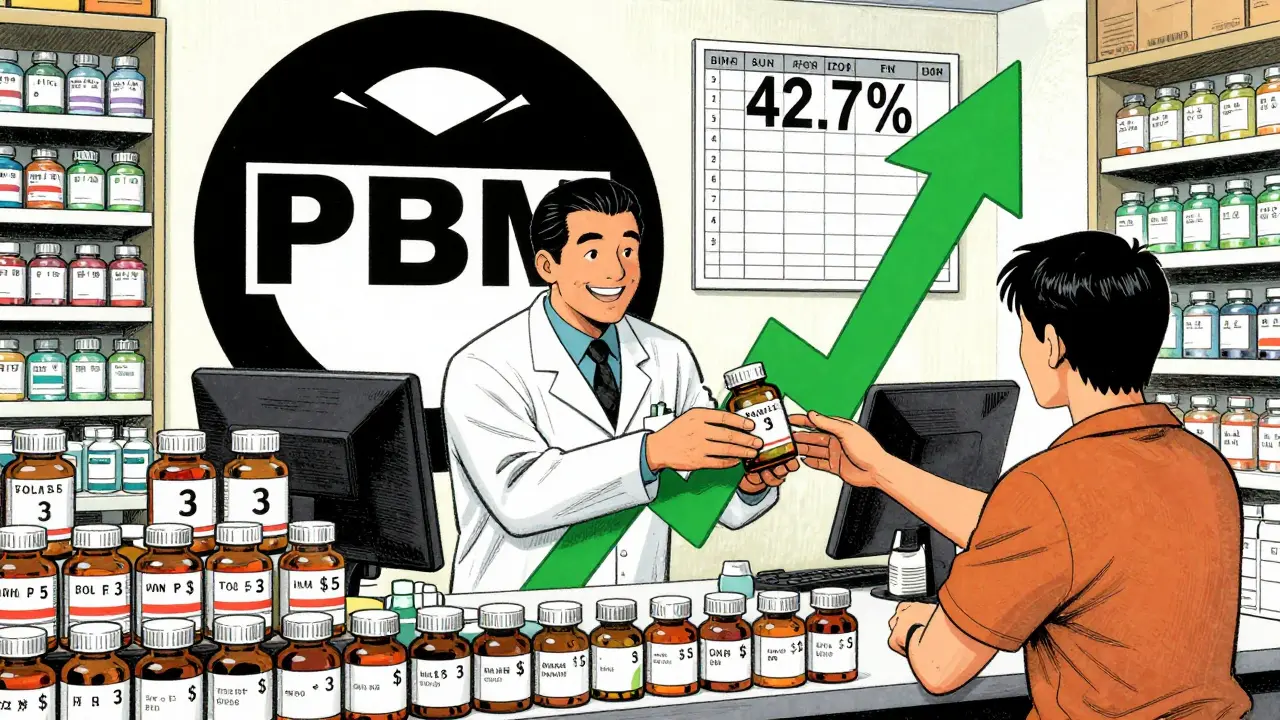

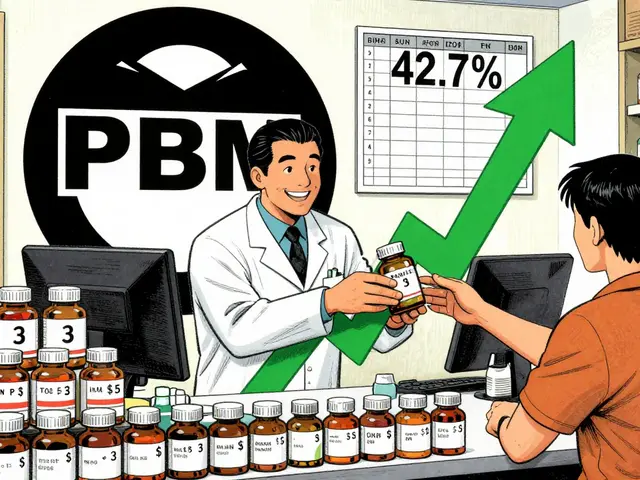

Pharmacies dispense about 90% of prescriptions as generics. That’s not because patients prefer them - it’s because insurance plans and pharmacy benefit managers (PBMs) force them. But here’s the twist: while generics make up 90% of prescriptions, they only account for about 25% of total drug spending. Brand-name drugs, which make up just 10% of prescriptions, soak up 75% of the money spent on prescriptions. So why are pharmacies making most of their profit from the cheap stuff? The answer is in the margins. Gross margins on generic drugs average 42.7%, according to the Schaeffer Center’s 2022 analysis. That means for every $100 a pharmacy collects for a generic drug, nearly $43 is profit before paying rent, staff, or utilities. For brand-name drugs? Just 3.5%. That’s not a typo. A $500 brand-name prescription might only net the pharmacy $17.50 in gross profit. But a $5 generic? That’s $2.14 in gross profit - and pharmacies sell hundreds of those every day. This isn’t about the price of the drug. It’s about the markup. Generic drugs are cheap to make - often under $1 per pill. But pharmacies are reimbursed based on a formula that sets a maximum allowable cost (MAC) by PBMs. Even when the drug costs 25 cents, the reimbursement might be $3. That’s a 1,100% markup. And since generics are dispensed so often, those small margins add up fast.The Real Money Flow: Who Gets What

The money from your prescription doesn’t just go from your insurance to the pharmacy. It passes through layers - manufacturers, wholesalers, PBMs, and finally the pharmacy. Each one takes a cut. And the cuts are wildly uneven. For brand-name drugs, manufacturers keep the lion’s share. They make about $58 in gross profit per prescription. PBMs get $8, wholesalers get $3, and pharmacies? Just $3. That’s why big pharma companies can afford billion-dollar ad campaigns. For generics, it flips. Manufacturers make only $18 per prescription. But pharmacies? They make $32. PBMs make $28. Wholesalers make $11. The pharmacy, which just fills the bottle, makes more than the company that made the drug. That’s the core of the paradox. And it gets weirder. Mail-order pharmacies - the ones that ship drugs to your house - make up to 1,000 times more margin on generics than a small-town pharmacy does. That’s because they negotiate bulk deals with PBMs and avoid the overhead of running a storefront. Independent pharmacies can’t compete with that.

Why Independent Pharmacies Are Struggling

There are about 22,000 independent pharmacies in the U.S. They make up 40% of all pharmacies, but they fill only 11% of prescriptions. Why? Because their margins are collapsing. Five years ago, many independents made 8-10% net profit on generics. Now, it’s down to 2%. Meanwhile, rent, insurance, staffing, and compliance costs have gone up 35%. A pharmacy owner in Ohio told Pharmacy Times he spends 15-20 hours a week just fighting with PBMs over reimbursement rates. That’s not time spent helping patients - that’s time spent trying to stay open. The problem isn’t just low reimbursement. It’s clawbacks and spread pricing. A PBM might tell the pharmacy it’s reimbursing $5 for a generic. But the PBM charges the insurance plan $8. That $3 difference is called “spread.” The PBM keeps it. Later, if the generic’s price drops to $4, the PBM might claw back $1 from the pharmacy - even though the pharmacy already paid the wholesaler. That’s like being paid for a job, then told you owe money because the boss got a better deal. The National Community Pharmacists Association (NCPA) found that 68% of independent pharmacy owners list declining generic reimbursement as their biggest threat. Between 2018 and 2023, 3,000 independent pharmacies closed. That’s not because people stopped needing meds. It’s because the system isn’t built to reward them.How Some Pharmacies Are Fighting Back

Not all pharmacies are going under. Some are changing how they make money. One strategy is ditching PBMs entirely. Pharmacies like Mark Cuban’s Cost Plus Drug Company charge $20 for a generic plus a $3 dispensing fee. No mystery. No clawbacks. You know exactly what you’re paying. It’s working - they’re filling over a million prescriptions a month. Others are shifting to medication therapy management (MTM). Instead of just handing out pills, pharmacists now sit down with patients to review all their drugs, catch interactions, and help with adherence. Medicare pays pharmacies for this service - sometimes $50-$100 per visit. That’s more than the profit from 50 generic prescriptions. Some pharmacies are becoming specialty pharmacies, handling complex drugs for conditions like cancer or rheumatoid arthritis. These drugs are expensive, but they come with higher reimbursement and fewer competitors. The trade-off? You need trained staff, special storage, and regulatory approvals. But the margins are steadier. A few are going direct-to-employer. Instead of working through insurance, they contract with local businesses to offer flat-rate pricing for common generics. It’s simple: $5 for metformin, $10 for lisinopril. No PBM. No spreads. Just fair pricing.

The Bigger Picture: Consolidation and Control

Three PBMs - CVS Caremark, Express Scripts, and OptumRx - control 80% of prescription transactions in the U.S. They’re not just middlemen anymore. They own pharmacies, own insurance plans, and own drug manufacturers. That’s vertical integration - and it gives them total control over reimbursement rates. The top five generic drug manufacturers now control 45% of the market, up from 32% in 2015. That means less competition. And less competition means higher prices. In some cases, when only one company makes a generic, the price goes up - even above the brand-name version. SureCost’s 2024 report found that for certain drugs, the single-source generic cost more than the brand. That’s not a market failure. That’s a system failure. The FTC has launched multiple antitrust investigations into generic drug makers over price-fixing. States like California, Texas, and Illinois have passed laws forcing PBMs to disclose how they set reimbursement rates. The Inflation Reduction Act’s drug price negotiation rules (starting in 2026) could lower overall spending - but it’s unclear if that will help small pharmacies or just shift the pain.What’s Next for Pharmacy Economics

The future of pharmacy profits won’t be about selling more pills. It’ll be about selling better service. Independent pharmacies that survive will be the ones that stop being just dispensers and start being health advisors. Those that cling to the old model - filling scripts, hoping PBMs pay enough - will disappear. The data is clear: generics are the engine. But the engine is sputtering. Without transparency, fair reimbursement, and competition, pharmacies won’t be able to afford the staff, space, or systems to serve patients properly. Some see this as a crisis. Others see it as an opening. For the first time in decades, patients are asking: Why does this cost so much? And more are willing to pay cash for transparent pricing. That’s a shift that could rewrite the rules - if pharmacies are ready to change with them.Do pharmacies make more money on brand-name drugs or generics?

Pharmacies make far more profit on generics. Even though brand-name drugs account for 75% of prescription spending, they contribute only 4% of pharmacy profit. Generics, which make up 90% of prescriptions, account for 96% of pharmacy profit. That’s because generic drugs have much higher gross margins - around 42.7% - compared to just 3.5% for brand-name drugs.

Why are generic drug margins shrinking even though they’re cheaper?

Margins are shrinking because pharmacy benefit managers (PBMs) are lowering reimbursement rates. Even though generics cost less to produce, PBMs set maximum allowable costs (MAC) that keep dropping. At the same time, operating costs like rent, staff wages, and compliance have gone up. Many pharmacies now make only 2% net profit on generics, down from 8-10% five years ago.

What are clawbacks and spread pricing?

Clawbacks happen when a PBM reimburses a pharmacy for a generic drug, then later demands money back because the drug’s price dropped. Spread pricing is when a PBM charges the insurance plan more than it pays the pharmacy - and keeps the difference as profit. For example, the PBM charges the insurer $8 for a drug but only pays the pharmacy $5, pocketing $3. Both practices squeeze pharmacy profits without transparency.

Can pharmacies survive without PBMs?

Yes, some already are. Pharmacies like Mark Cuban’s Cost Plus Drug Company and others using direct-to-consumer or direct-to-employer models bypass PBMs entirely. They charge transparent prices - like $20 plus a $3 fee - and avoid clawbacks and spread pricing. These models are growing, especially as patients become more cost-conscious and demand clear pricing.

Why do mail-order pharmacies make so much more on generics?

Mail-order pharmacies operate at massive scale and negotiate bulk deals with PBMs. They also avoid the overhead of physical stores - no rent, fewer staff, lower insurance costs. For certain drugs, they make up to 1,000 times more margin than a small retail pharmacy. This gives them a huge advantage, making it nearly impossible for independents to compete on price alone.

So let me get this straight - pharmacies make more off $5 generics than $500 brand names because PBMs are literally printing money while pharmacists starve? Brilliant. The entire system is a rigged casino where the house always wins and the dealer gets fired for losing. 🤡

PBMs are the real villains. No one talks about clawbacks. They take your money then come back for more. It's predatory.

This isn’t economics - it’s institutionalized theft disguised as market efficiency. PBMs are rent-seeking monopolists with regulatory capture. The fact that you’re surprised by this proves you’ve never read a single antitrust filing. The system was designed this way. It’s not a bug. It’s a feature.

Pharmacists are just glorified cashiers. If they can't handle the margins, they shouldn't be in business. This isn't a crisis - it's Darwinism. The weak get weeded out. End of story.

I just want to say thank you for writing this. 🙏 It’s so frustrating how no one talks about how pharmacies are being strangled by PBMs. I’ve seen my local pharmacy struggle for years. They deserve better 💔

Mark Cuban’s model? Cute. But it only works because he’s rich enough to lose money on it for PR. The rest of us don’t have a billion-dollar ego to fund our moral superiority.

The structural arbitrage here is fascinating - a classic case of margin compression inverted by volume elasticity. PBMs exploit MAC pricing algorithms to extract surplus value from high-frequency, low-cost transactions while suppressing wholesale competition. The result? A Pareto-optimal outcome for intermediaries, but a negative-sum game for local providers. What’s missing is the institutional feedback loop: when reimbursement rates are algorithmically dictated, pharmacies lose agency to adapt. They’re not just underpaid - they’re disempowered.

I run a small pharmacy in rural Ohio. We’ve started doing MTM sessions - Medicare pays $75 per visit. We’re not making bank, but we’re finally doing what we went to school for: helping people. It’s not glamorous, but it’s honest. And honestly? That’s worth more than a 42% margin on a $3 pill. 🙌

It’s ironic. We treat medicine like a commodity, but then act shocked when the system dehumanizes the people who deliver it. Maybe the real question isn’t how to fix margins - but whether we should be treating health like a supply chain at all.

The data presented is statistically sound and methodologically rigorous. The systemic issues outlined - clawbacks, spread pricing, vertical integration - are well-documented by the GAO, CBO, and FTC. To dismiss this as anecdotal is to ignore empirical evidence. The U.S. healthcare system is not broken. It is functioning exactly as designed - to enrich intermediaries at the expense of providers and patients.

Ah yes, the classic ‘pharmacist as hero’ narrative. Let’s not pretend these are saints. Many of them are just lazy entrepreneurs who didn’t want to work a real job. If you can’t compete with mail-order giants, maybe you should’ve invested in logistics, not just a counter and a bottle of Tylenol.

i read this whole thing and just want to say… i had no idea. my grandma’s pharmacy shut down last year and i thought it was just because she retired. now i get it. thank you for explaining it so clear. i’m gonna tell everyone i know.

There’s a quiet revolution happening. Pharmacies that treat patients as humans, not transactions, are thriving. We offer free blood pressure checks, medication sync, even tea and cookies while you wait. It’s not about the pill - it’s about the presence. And people notice. The system wants you to be a machine. Don’t be. Be a healer.

The future of pharmacy lies in value-based care. Transitioning from volume-driven dispensing to outcomes-driven counseling is not optional - it is existential. Regulatory alignment, reimbursement reform, and professional rebranding must occur simultaneously. Failure to adapt constitutes professional negligence.